February 2025

Demonstrating progress towards corporate climate goals

This guidance is based on the Value Change Initiative (VCI) working group output “Accounting and reporting Scope 3 Interventions in the Food and Agriculture sector”.

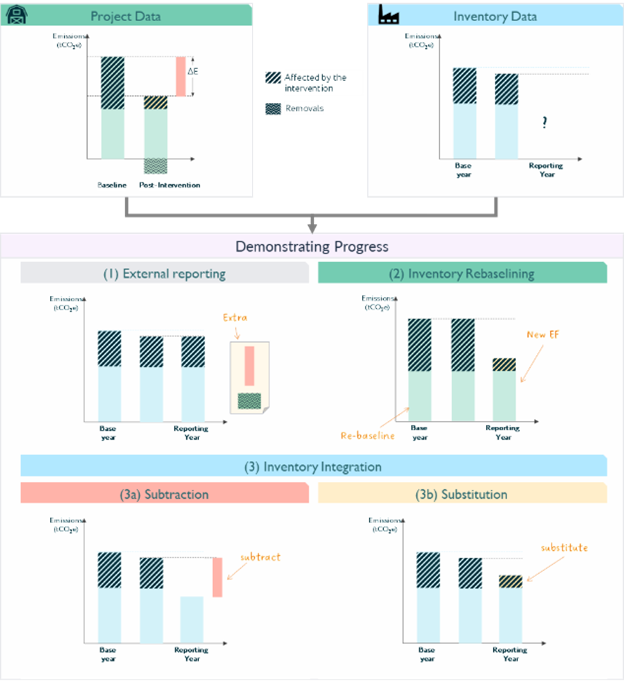

To demonstrate progress towards their climate goals, companies need to lower their own emissions as well as those occurring in their value chains. These emissions are accounted for as Scope 3 emissions in the Greenhouse Gas (GHG) inventory of companies, which involves using an emission factor linked to a particular activity, such as the purchasing of goods and services. Often, the emission factors used in Scope 3 inventories are based on secondary data derived from generic Life Cycle Assessment (LCA) databases, representing an average factor on a national or even global level. Consequently, the calculation of a company’s emissions follows inventory accounting and focuses on year-to-year changes in the inventory (see top right box in Figure 1).

Measuring progress solely using generic LCA data is challenging, as updates are not frequent, and the impact of partial best practice can be lost in the mix. A more effective way to ensure value chain decarbonization is to implement specific interventions in known emissions hot spots. Depending on the site, these interventions can lead to substantial reductions and removals of emissions. Project accounting is used to compare post-intervention emissions to a counterfactual baseline, resulting in a project specific delta. This results in mitigation outcomes, which measure the targeted improvements in operations affected by the intervention (see top left box in Figure 1).

However, corporate climate goals are measured using inventory, not project accounting. This creates a disconnect when reflecting these mitigation outcomes in corporate Scope 3 inventories. The main question is whether the reductions or the resulting emission after the implementation of the intervention, should be considered. The next section discusses different approaches, their mechanisms, characteristics and compliance with existing reporting frameworks are discussed.

It should be noted that compliance with existing inventory accounting frameworks, such as the upcoming GHG Protocol Land Sector and Removals Guidance (LSRG), is also subject to other eligibility criteria, such as traceability requirements, defined boundaries, and scope of the emission factor (EF), as well as allocation factors. For simplification, the assessment of the compliance of the four approaches presented assumes these additional criteria are met, therefore focusing mainly on the mechanism of data transfer or integration between intervention and inventory data.

Approaches to demonstrate progress

In theory, there are four approaches available to demonstrate progress from value chain interventions. It is important to note that not all of these approaches are in alignment with requirements from standards such as GHG Protocol.

1) Report mitigation outcomes outside of the inventory,

2) Update the inventory with a new complete EF

3) Subtracting project specific reductions from current inventory EF

4) Substituting affected project emissions inside current inventory EF

Figure 1 shows the mechanism and specific data used for each of the respective approaches.

Except for external reporting, it should be mentioned that a retroactive rebaselining of the base year data could be required to ensure that the data is comparable year-on-year.

Caption: Figure 1 Overview of main data points from intervention (green and yellow) and inventory (blue) and the potential approaches (1-4) to demonstrate progress towards climate goals. Hatched areas represent the emissions affected by the intervention.

1. External reporting

The first approach involves the reporting of mitigation outcomes outside of the Scope 3 inventory (see External Reporting box in Figure 1). Various options exist, ranging from reporting as separate line item, to narrative claims, to demonstrating progress within a given performance framework. This approach significantly reduces complexity, as no calculation in the inventory is required, and the achieved mitigation outcomes are accurately reflected. However, except for removals, it is unclear how these achieved mitigation outcomes can count towards corporate climate goals, as fungibility criteria for insetting credits and additional guidance on potential performance frameworks are still not defined by the standards.

2. Update EFs in the inventory

The second approach is the updating of inventory emissions based on a new and complete EF gathered from the intervention sites (see Update EF box in Figure 1). This involves compiling the entire life cycle emissions of a specific site and updating them in the inventory. This approach aligns with reporting frameworks but can lead to very high data requirements and more accurate data does not necessarily mean lower emissions, if no rebaselining is applied.

3. Subtraction

Subtraction reduces the affected emissions by the difference between baseline and post-intervention emissions, representing the emission reductions achieved by the intervention (see Subtraction box in Figure 1). This can be applied to the overall inventory or limited to the affected operation. While subtraction has the advantage of a simple calculation and the reflecting of mitigation outcomes, it also can lead to artificially low or even negative EFs, if baseline and inventory data are not well aligned. Subtraction is not in compliance with existing reporting frameworks (such as GHG Protocol) and could therefore only be used outside of it.

4. Substitution

Substitution is an inventory accounting method that enhances accuracy by integrating primary data. It does so by isolating individual components of an emission factor and replacing average base-year data with more precise, value chain-specific estimates for a given year (see Substitution box in Figure 1). In this approach, annual emissions measured after the implementation of an intervention directly replace their corresponding counterparts in the inventory.

Substitution aligns with the hybrid inventory accounting methodology, where secondary data is replaced by more accurate, primary data collected from intervention sites. While this approach preserves measured emissions, it may require more complex modeling and disaggregation of the inventory’s emission factors. Additionally, substitution can lead to increased emissions in the inventory for high emission sites. For substitution to be integrated in inventory accounting, the accounted goods must meet the GHG Protocol LSRG requirements for traceability, spatial boundaries and what the EF represents.

Conclusion and outlook

In conclusion, the four approaches presented allow reporting companies to demonstrate progress from value chain interventions towards their corporate climate goals. Except for removals, there is unclear guidance on how to report mitigation outcomes outside of the inventory. Generating new and complete emission factors aligns with reporting frameworks but can entail high data requirements and can lead to higher emissions. Subtraction of mitigation data directly in the inventory is currently not compatible with existing reporting frameworks. Substitution aligns with the hybrid approach for inventory accounting but might require additional inventory adjustments for high emission sites. In the future, clearer guidance is required from the existing reporting frameworks to determine which approach can be used for demonstrating progress on value chain decarbonization through intervention outcomes.

SustainCERT’s value chain interventions and emission factor verification and resulting Impact Units are designed to ensure that all the project-specific data required for any of the four approaches is available and can be used by corporates to demonstrate progress towards their climate goals.

Credibly demonstrate progress toward climate targets

Get in touch with our team to find out how SustainCERT can help you verify and report the impact of your value chain interventions.