September 2024

Dual factor verification ensures credible Scope 3 reporting and co-claiming

Tackling Scope 3 emissions is crucial for companies aiming to achieve global net-zero targets in the coming decades. However, the complex nature of the value chain emissions presents numerous challenges. The lack of clear regulations is stalling investments in upstream interventions, while difficulties in tracking and allocating emission reductions across various goods and actors in the value chains are leading to unclear incentives. Further blockers to scaling value chain decarbonization efforts include the volatility of value chains, the risk of freeriding, and double counting issues.

Even after companies and suppliers implement interventions, accurately claiming and reporting mitigation outcomes in an inventory requires adjusting for different accounting methodologies, such as project-based/intervention and inventory accounting. This is essential for companies to report on year-on-year changes in their inventory.

To address these challenges, SustainCERT has developed a dual factor credibility framework, which allows companies to 1) verify mitigation outcomes and 2) unitize, transfer, credibly claim and report emission reductions in a Scope 3 inventory. Put together, this can help your company decarbonize your value chain, meet Scope 3 targets, and collaborate with partners in the value chain to share costs. Read on to understand how each stage of the verification works and why they are important for credible Scope 3 reporting.

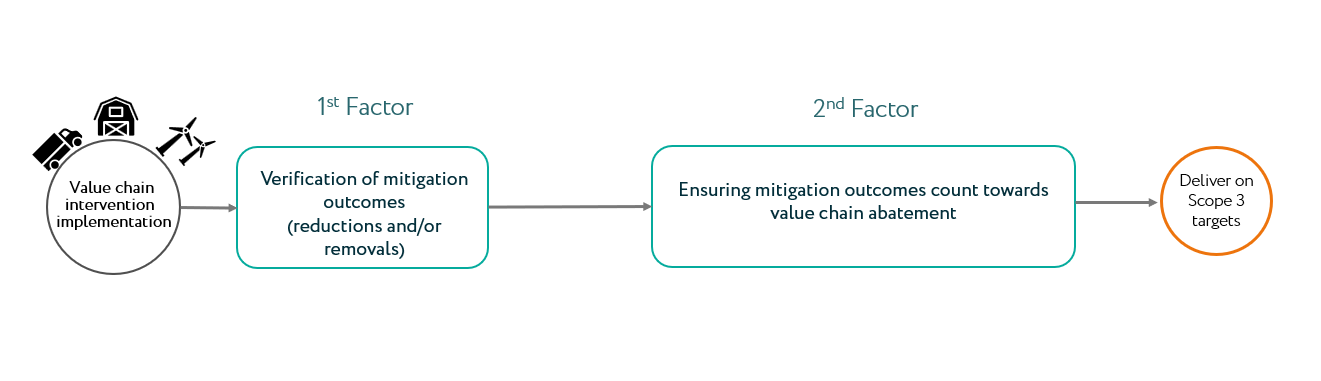

1st Factor: Verify your mitigation outcomes

The 1st factor verification allows your company to demonstrate emission reductions are actually happening in your value chain, and that your company is enabling them.

The process starts with implementing an intervention, such as a new technology or process change, in your value chain. For example in agriculture, an intervention might be reduced fertilizer use to decrease emissions. During the implementation phase, you should collect project data such as the volume of product affected and measured data for the baseline.

This data is then used to verify the mitigation outcomes in the 1st Factor. This includes an audit against the SustainCERT Rules & Requirements, assessing the greenhouse gas (GHG) quantification approach and the project data, and assigning ownership of the mitigation outcomes.

The review focuses on the following aspects:

- Chosen methodologies

- Quantification approach

- Proposed baseline

- Assessment of the uncertainty and data quality/management

Assignment of ownership entails assuring that the involved parties have granted the exclusive rights-to-report the resulting mitigation outcomes to the company in question. This is done to avoid double counting. In this step, it’s possible to split the mitigation outcomes between different co-investors.

After a successful completion of the 1st Factor, the company receives a verification statement which can feed into a Scope 3 report.

2nd Factor: Credibly report and co-claim your Scope 3 emission reductions

After the mitigation outcomes have been verified, companies can continue the process to credibly co-claim the outcomes together with partners, and report in line with standard accounting frameworks (e.g., GHG Protocol Scope 3 Standard). This is done through the 2nd Factor, which allows companies to share the value of interventions through Impact Units.

The 2nd Factor includes the following 3 steps:

- Attribution to value chain

- Assessment of claim and right to report

- Reporting impacts in an inventory

Attribution to value chain

Attributing the intervention outcomes to a value chain ensures that companies are able to only claim impacts that are within their value chain, consisting of the correct Impact Layer and Supply Shed. This equips companies to follow the Science Based Targets initiative mitigation hierarchy by focusing their efforts on reducing or removing emissions directly in their value chain.

The GHG outcomes of an intervention are unitized and registered as Impact Units. To ensure credible co-claiming of GHG outcomes across the value chain, Impact Units are issued at different stages of the value chain called Impact Layers, linking the mitigation outcomes to the actor’s position in a specific value chain. The main layers are raw material production, mid- and end-product processing as well as wholesaler and retailer.

Finally, GHG mitigation outcomes are assigned to a specific Supply Shed, which represents a common market to exchange service equivalent goods. This means that even when traceability to farm-level is not feasible, companies can report emission reductions based on investments made within the Supply Shed where they source. This enables companies to de-risk the volatility of value chains and provides additional return on investment by enabling transfers across the value chain.

Impact Units can be transferred to different actors in the same value chain, allowing companies to share the costs of interventions. They are tracked in a public registry to enhance transparency, reducing the risk of freeriding and double counting.

Assessment of claim and right to report

After exchanging Impact Units with different actors in the value chain, companies can claim the underlying mitigation outcomes for their own reporting.

It’s important to note here what good or commodity was impacted by the intervention, and what is the purchased good that is linked to the claim. For example, if an intervention takes place on a dairy farm impacting milk, companies down the value chain such as a cheese manufacturer or a retailer selling cheese may wish to claim these mitigation outcomes. This needs to be considered in the emission factors used in the calculations.

In this step, there is also a check on proof of sourcing. This means that a company needs to demonstrate that it is sourcing a specific volume of goods from the relevant Supply Shed. The amount of Impact Units a company can claim is always linked to the amount of goods that it sources – it can’t claim emission reductions beyond this volume because the actual goods are sourced by someone else.

Reporting impacts in an inventory

The accounting methods for interventions and inventories are different. This means that when intervention accounting is used to track changes in emissions from a specific project, these calculations must be adjusted to the correct format when integrating them into the Scope 3 inventory. The most important element is to ensure that the scope and boundaries of the existing inventory items (i.e., emission factors) are respected when integrating the mitigation outcomes. Integrating and recalculating emissions data in the inventory enables credible reporting of year-on-year improvements in a Scope 3 report.

After the completion of the 2nd Factor, companies can credibly report the emission reductions taking place in their value chains, as well as co-claim those impacts together with partners in their value chain.

The dual factor framework addresses common challenges caused by the complexity of value chains and the associated accounting methods, giving companies the confidence to report verified outcomes, collaborate with value chain partners, and co-claim impacts. The possibility to share the cost of interventions across the value chain and be recognized for the generated impact through co-claiming enables companies to scale action. Check out our new paper for more details on the dual factor credibility framework.

Ready to verify, report and co-claim Scope 3 emission reductions?

SustainCERT’s value chain impact verification solution has all the features of the dual factor verification built-in, allowing for seamless reporting and co-claiming of verified Scope 3 emissions.